Health Care Reform: Marketplace Subsidies, Medicaid and CHIP

Posted by Anna Koehler on Dec 3, 2014 in Health Insurance News

Under the Affordable Care Act (ACA), uninsured individuals are required to buy insurance or face a tax penalty. When you use a health insurance Marketplace, you may be able to get lower costs on monthly premiums or out-of-pocket costs, or get free or low-cost coverage. Subsidized coverage—or coverage that’s obtained through financial assistance from programs to help people with low and middle incomes—is available to individuals and families with household incomes up to 400 percent of the federal poverty level and who are not offered affordable coverage through their employers.

You can save money in the Marketplaces three ways. All of them depend on your income and family size.

1. You may be able to lower costs on your monthly premiums through tax credits when you enroll in a private health insurance plan.

2. You may qualify for lower out-of-pocket costs for copayments, coinsurance and deductibles.

3. You or your child may get free or low-cost coverage through Medicaid or the Children’s Health Insurance Program (CHIP).

Subsidized coverage may be available to individuals and families with household incomes up to 400 percent of the federal poverty level and who are not offered affordable coverage through their employers.

Tax Credits for Premiums

The most widely available subsidy is the Advance Premium Tax Credit, which helps cover the gap between the cost of their premium and what they can afford to pay.

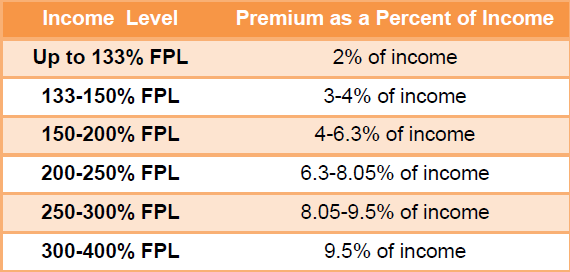

The ACA requires households participating in the Marketplaces to put a certain percentage of their income toward the cost of health insurance. The exact percentage households need to pay is graduated up to 400 percent of the federal poverty level (FPL), with people at that percentage level required to pay the most and people at 100 percent of the federal poverty level required to pay the least. A rough guide to the graduated percentage is as follows:

Source: Kaiser Family foundation

Source: Kaiser Family foundation

Health Care Reform: Marketplace Subsidies, Medicaid and CHIP

The percentage of income that households are required to pay, however, may not be enough to cover the cost of the insurance policy. The Advanced Premium Tax Credit steps covers the amount between what households are required to pay and the cost of the insurance policy. Premium tax credits are both refundable and advanceable. A refundable tax credit is available to a person even if he or she has no tax liability. An advanceable tax credit allows a person to receive assistance at the time that he or she purchases insurance rather than paying his or her premium out of pocket and waiting to be reimbursed when filing an annual income tax return. There are several online calculators available to help you estimate the size of your premium tax credit. In general, people at the following income levels will qualify to save in 2015.

• $11,670-$46,680 for individuals

• $15,730-$62,920 for a family of two

• $19,790-$79,160 for a family of three

• $23,850-$95,400 for a family of four

• $27,910-$111,640 for a family of five

• $31,970-$127,880 for a family of six

• $36,030-$144,120 for a family of seven

• $40,090-$160,360 for a family of eight

Reduced Out-of-pocket Costs

In addition to the Advance Premium Tax Credit, households that earn up to 250 percent of the federal poverty level may be eligible for cost-sharing subsidies. These

subsidies are designed to help lower out-of-pocket costs. Health insurance companies offering coverage through the Marketplace must lower the amount you pay out of pocket for essential health benefits if your household income is within the following amounts.

• $11,670-$29,175 for individuals

• $15,730-$39,325 for a family of two

• $19,790-$49,475 for a family of three

• $23,850-$59,625 for a family of four

• $27,910-$69,775 for a family of five

• $31,970-$79,925 for a family of six

• $36,030-$90,075 for a family of seven

• $40,090-$100,225 for a family of eight

Reduced cost-sharing is only applicable to silver plans. If you qualify for out-of-pocket savings, you must choose a silver plan to get the savings.

Medicaid Eligibility

Medicaid is the nation’s health insurance program for low-income individuals and families. To qualify for Medicaid, individuals must be low-income or must have incurred health expenses that have caused them to “spend down” their incomes to Medicaid eligibility levels.

Under the ACA, states have the option of expanding Medicaid to households making up to 138 percent of the poverty line. However, these are the minimum thresholds for Medicaid expansion. The rules for Medicaid eligibility are different for each state. States can choose to offer Medicaid to households with a higher income. Conversely, states can choose not to participate in the Medicaid expansion.

If your state is expanding Medicaid, you may qualify for Medicaid coverage if your annual income is lower than the numbers listed below.

• $16,105 for an individual

• $21,707 for a family of two

• $27,310 for a family of three

• $32,913 for a family of four

Health Care Reform: Marketplace Subsidies, Medicaid and CHIP

• $38,516 for a family of five

• $44,119 for a family of six

If your state is not expanding Medicaid, you may not qualify for a Marketplace savings program if your annual income is less than the amounts below.

• $11,670 for an individual

• $15,730 for a family of two

• $19,790 for a family of three

• $23,850 for a family of four

• $27,910 for a family of five

• $31,970 for a family of six

To determine your eligibility for Medicaid under the ACA, visit your state’s Medicaid Web page.

CHIP Eligibility

CHIP provides low-cost health coverage to children in families that earn too much money to qualify for Medicaid. In some states, CHIP covers parents and pregnant women. Each state offers CHIP coverage and works closely with its state Medicaid The benefits covered through CHIP are different in each state, but all states provide comprehensive coverage, including:

• Routine check-ups

• Immunizations

• Doctor visits

• Prescriptions

• Dental and vision care

• Inpatient and outpatient hospital care

• Laboratory and X-ray services

• Emergency services

States may choose to provide additional CHIP benefits. Check with your state for more information about covered services. Each state program has its own rules about who qualifies for CHIP. To see if you or your children qualify, visit www.insurekidsnow.gov.

For more information about individual insurance and health care reform, or for help

getting started, contact Koehler, Koehler Inc. today.

source: Healthcare.gov